The B2B tech market is in constant flux. For marketers, understanding what your audience is thinking and doing is critical to cutting through the noise.

Each month, we explore the issues shaping real-world technology decisions, drawing on insight from 100 IT leaders in our expert network, the Vanson Bourne Community.

Welcome to the first edition of Signals.

This month, we set out to understand:

• How the disruption of 2025 is reshaping technology purchasing in 2026

• Where AI plans stand today and where it is delivering measurable value

• How organisations are funding their AI ambitions

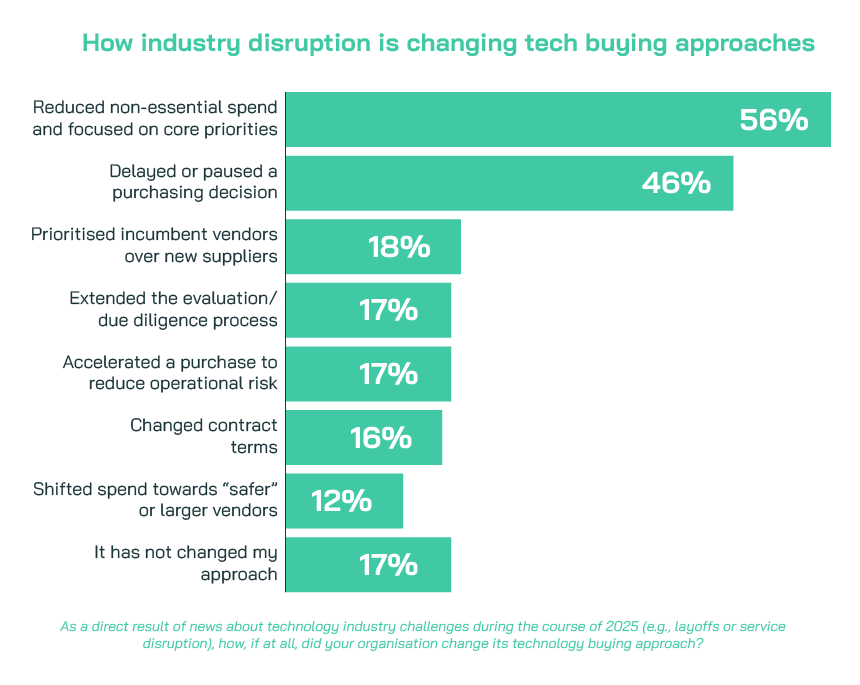

A defensive turn in technology buying in 2026?

In early 2025, our AI: The Race for a Use Case report highlighted the uncertainty that organisations are facing when it comes to their AI plans and their struggles in seeing clear value from what AI can deliver. As we move through 2026, that uncertainty has hardened into caution.

News of layoffs and service disruption hit the headlines throughout 2025, from headcount reductions at Google, AWS and SAP to high-profile outages affecting services such as Microsoft 365 and Azure. It’s clear that IT leaders have had little respite from news questioning vendor stability, so we wanted to explore whether that’s impacting their technology purchasing approach in 2026.

One clear theme emerged from what they told us: caution is rising. Over half (56%) say they have reduced non-essential spend and focused on core priorities as direct results of this disruption. Almost half (46%) have delayed or paused a purchasing decision. Meanwhile, 17% have extended due diligence processes and a similar proportion (18%) are prioritising incumbent vendors over new suppliers.

This is classic risk containment behaviour. As one IT leader in the construction and property sector told us:

“Beyond a doubt the greatest pressure is constrained budget spend so we are halting non-essential spend and deferring some projects.”

For marketers, the signal is clear: the buying climate is cautious in 2026. Communicating stability, measurable ROI and risk mitigation matter more than ever and will form a key part of what sets one brand apart from another in buyer minds.

And yet… AI is not slowing down

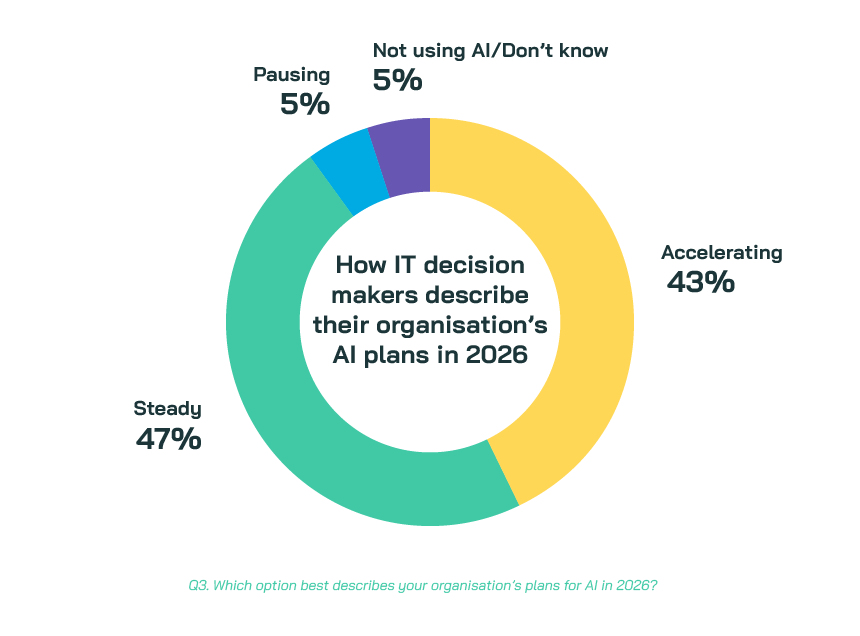

Despite this defensive posture, AI plans remain robust. Over four in ten (43%) say their organisation is accelerating AI in 2026, and a further 47% say plans are steady. Only 5% are pausing, and none are scaling back.

As we’ve just seen, while caution is shaping spending plans, AI investment is not being treated as discretionary. It is being protected.

There is another force at play here too: competitive anxiety. Recent commentary in the tech press has highlighted how organisations feel they cannot afford to fall behind in the AI race, even if the business case is still evolving. This theme was also uncovered in our Mind the Gap research collaboration with Tech Funding News and Liberty Comms, exposing senior leader fears in the UK’s ability to compete on the global stage.

But far from such fears putting the brakes on plans, instead they appear to be fuelling them. In a year where disruption is causing 56% to cut non-essential spend and 46% to delay purchases, AI is the exception. It is being ringfenced, accelerated, or at the very least maintained.

But the story isn’t one of unchecked expansion. While the eagerness to adopt AI remains, questions linger on exactly where it can help (we’ll explore that more in the next section). As one public sector ITDM respondent put it:

“AI seems to be the answer to everything without knowing the question.”

The tension between urgency and uncertainty helps explain why the AI initiatives delivering the clearest value today are pragmatic rather than transformational.

Where AI is actually delivering value

The ITDM insights featured in our AI: The Race for a Use Case report last year delivered a clear message to vendors: show us real value. While many were trialling or using AI on an ad-hoc basis in pockets of the business, most (69%) believed that AI wasn’t currently capable of delivering (marketers take note here) “what the marketing promises”.

A year on, we wanted to uncover if this remains the case by asking where AI is delivering measurable value today.

The most common themes? Time saving, automation and coding efficiency.

“Time saved doing admin.” (ITDM, construction and property sector)

“Copilot is a valuable time saving resource right now for meeting summaries and any form of process documentation.” (ITDM, public sector)

“AI driven Chatbots and the use of AI in programming are showing some measurable value today.” (ITDM, financial services sector)

In operational environments, the return appears even clearer based on one respondent from the energy, oil and gas sector:

“AI-driven predictive maintenance is delivering the most measurable value by reducing downtime and operational costs through early detection of equipment failures.”

It all points to augmentation, rather than revolution. AI is helping existing teams move faster and avoid additional hiring, rather than reinventing entire business models.

But there is a strategic tension here. Productivity gains are easier to measure and justify in a defensive spending climate. True strategic shifts require upfront investment, organisational change and longer time horizons. In a cost-conscious market those bets are harder to make.

The risk is that AI becomes a layer of efficiency on top of legacy complexity, rather than the catalyst for structural change. As McKinsey’s latest State of AI research shows, only 39% report EBIT impact at enterprise level and the organisations capturing disproportionate value are those pursuing growth and innovation, not just efficiency.

The impacts on purchasing approaches and the apparent commitment to AI investment that we’ve seen, lead us to our final area to explore…

How are AI plans being paid for?

AI may be protected but of course it isn’t free. And so the trade off emerges, with most organisations not funding AI with entirely new money. Instead, they are reallocating.

“Our AI efforts this year are mainly being funded with the technology budget.” (ITDM, business and professional services sector)

“AI initiatives are mainly being funded by a reduction in staff which has delivered savings in terms of salary cost, pension cost, national insurance and benefit cost and the move to more centralised office space. Also the increased use of cheaper offshore resource. All these savings are being channelled into AI development and rollout.” (ITDM, financial services sector)

“We are funding AI by shifting money from lower priority projects, especially legacy upgrades and experimental side projects.” (ITDM, retail, distribution and transport sector)

In other words, AI investment is often being offset by deferred modernisation, tighter headcount control, or the scaling back of non critical initiatives. One respondent from the retail, distribution and transport sector captured the tension succinctly:

“Budget constraints have pushed back a number of nice to have modernisations. As a result, legacy IT and technical debt keep getting de-prioritised.”

AI is accelerating, but it is being funded by squeezing elsewhere. The question for leaders is whether short-term efficiency gains today are creating the headroom for deeper reinvention tomorrow or simply masking postponed transformation.

For marketers, all of this shapes the type of AI story that will resonate in 2026: not just faster processes, but credible pathways from operational wins to strategic impact.

Key takeaways for tech marketers

1. The market is risk averse. With 56% cutting non-essential spend and 46% delaying purchases as a direct result of news about technology industry challenges in 2025, your messaging must help buyers justify investment in a climate of scrutiny

2. Right now, the clearest AI returns are coming from productivity gains. In a defensive spending climate, efficiency evidence travels further than transformational promises

3. Remember that every AI proposal competes internally with legacy upgrades, hiring and other projects. If you’re not clearly articulating short term, defensible value, it may not survive internal reallocation debates

Signals is our regular snapshot of what IT leaders are prioritising right now. Each month, we survey 100 UK IT decision makers across sectors, from organisations with 100+ employees. All are members of our expert network, the Vanson Bourne Community, giving you direct insight from the humans at the heart of tech.

If you’d like to explore how these shifts are playing out in your sector, or go deeper into the data behind this edition, we’re always happy to continue the conversation.